The next-generation direct debit

payment solution

Response within 24 hours !

mandates

with no limit

no hidden fees

A complete solution

for your customer payments

Response within 24 hours !

Your entire sample collection process, fully digital

One-time direct debit

Subscription

Installment

Automated direct debit

management

Creating and signing e-mandates

Dynamic notifications

Automated tracking

Programmed retry

Response within 24 hours !

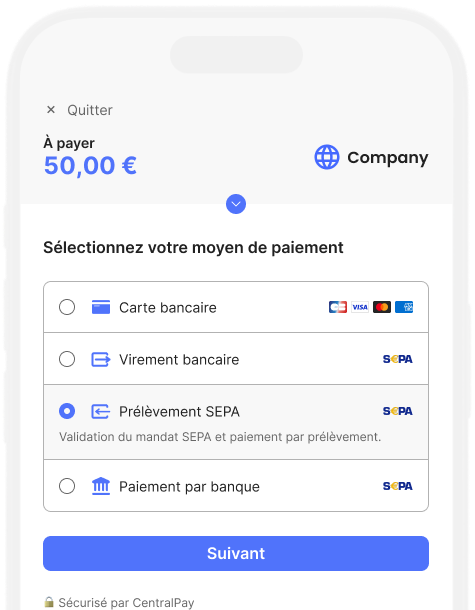

SEPA Direct Debit

for each business context

Collect payments and pay your merchants

- Express onboarding for your merchants

- Payment orchestration managed by CentralPay

- Marketplace commission collection management

- Automated payouts

Accept more online payments

- Boost card payments with Apple Pay and Google Pay

- Accept instant bank transfers, Pay by Bank and SEPA direct debits

- Quick integration via plugin, SDK or hosted payment page

- Integrated data security and anti-fraud services

Get your bills paid, effortlessly

- Payment requests via email & SMS, with automatic reminders

- Automatic processing of transfers, direct debits and cards

- Cash payments, down payments and payments due

- Synchronization with ERP systems, software and business tools

Deploy complex models, simply

- Crypto-Asset Service Providers (MiCA): Fiat-to-Crypto payment rails →

- Crowdfunding (PSFP): regulated fundraising and disbursements →

- Software publishers: partner model and rapid integration →

- Specific project: scoping and support by experts

FAQs

Questions about direct debit payment solutions?

SEPA Direct Debit (SDD) is suitable for any business that collects recurring or deferred payments: subscriptions, membership fees, rent, B2B invoices, etc. With CentralPay, manage mandates, due dates, rejections, reconciliations, and refunds from a single platform.

SEPA Core Direct Debit applies to both individuals and businesses. It allows the payer to dispute the direct debit up to 13 months after collection. SEPA B2B Direct Debit is used by public institutions to collect payments from businesses, as these payments cannot be disputed.

A customer has 13 months from the date the account is debited to contest a direct debit payment. In this case, the merchant will have to pay a fee of up to €20 to cover those charged by CentralPay's bank for each refused transaction.