A card payment solution,

designed for the user experience

Accept card payments online. Benefit from innovative features and advanced, built-in security protocols, all from a single provider.

Response within 24 hours !

card payments

transaction fees

certified environment

A complete solution

for your card payments

Response within 24 hours !

All card facilities, easily accessible

Card payment

Accept bank cards (CB, Mastercard, Visa, and American Express), benefit from innovative features (subscription, secure imprint, or pre-authorization), and native security protocols.

Apple Pay and wallets

Activate Apple Pay and Google Pay in just a few clicks. Offer your customers mobile payments without entering card numbers. Available across all your payment channels, both online and in-store.

Card subscription

Set up credit card payments without requesting payment details for each payment due date. Define the frequency, amount, and duration. Manage automatic reminders in case of payment failure.

Card imprint

Save your customers’ card details to facilitate future purchases. Collect payments in one click, without re-entering information. Ideal for subscription services and recurring sales.

Pre-authorization and deposit

Hold an amount on your client’s card without immediately charging it. Confirm or cancel the transaction depending on the outcome of the service. Ideal for rentals, hotels, and services requiring a security deposit.

Card payment,

at the right time

online, remote, in-person, or hybrid.

All your card payment data is centralized and reconciled in real time.

You benefit from a consolidated view to manage your business without juggling multiple tools.

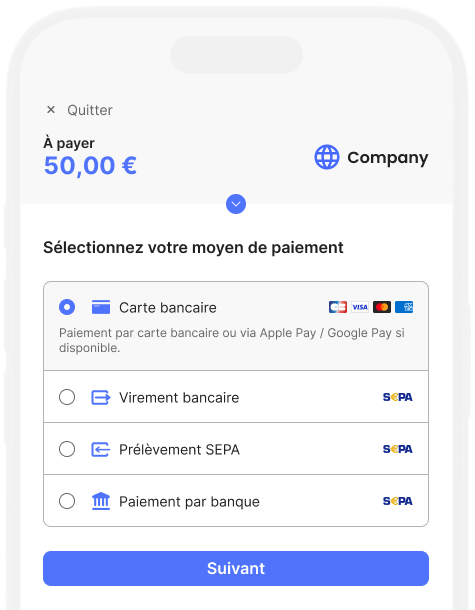

Online payment

Customize your payment page and integrate it into your e-commerce site or share it in your customer communications.

Payment by email and SMS

Edit your email, SMS, or QR code payment link templates. Send them on a one-off basis or schedule them.

Proximity payment

Accept payment from your customers by card or Pay by Bank, either at your payment terminal (POS) or directly from your smartphone.

Response within 24 hours !

Le paiement par cartepour chaque contexte métier

Collect payments and pay your merchants

- Express onboarding for your merchants

- Payment orchestration managed by CentralPay

- Marketplace commission collection management

- Automated payouts

Accept more online payments

- Boost card payments with Apple Pay and Google Pay

- Accept instant bank transfers, Pay by Bank and SEPA direct debits

- Quick integration via plugin, SDK or hosted payment page

- Integrated data security and anti-fraud services

Get your bills paid, effortlessly

- Payment requests via email & SMS, with automatic reminders

- Automatic processing of transfers, direct debits and cards

- Cash payments, down payments and payments due

- Synchronization with ERP systems, software and business tools

Deploy complex models, simply

- Crypto-Asset Service Providers (MiCA): Fiat-to-Crypto payment rails →

- Crowdfunding (PSFP): regulated fundraising and disbursements →

- Software publishers: partner model and rapid integration →

- Specific project: scoping and support by experts

FAQs

Questions about the credit card payment solution?

Our online card payment fees adapt to your business volume, while remaining simple and cost-effective.

Simulate your pricing on our pricing page.

CentralPay offers you a complete infrastructure to manage all your card payment scenarios via a hosted page or API, remote payment by credit card via email or SMS, in-store or mobile payment. Each transaction relies on a secure payment environment certified PCI-DSS Level 1, with integrated strong authentication (3DS2), to protect your customers without hindering their experience.

When disputing a card payment, CentralPay supports you every step of the way: you are notified in real time, you can submit your evidence directly from the platform, and our teams guide you through the dispute process. To minimize disputes proactively, our card payment system integrates fraud detection tools and requires 3DS2 authentication for high-risk transactions, significantly reducing the risk of chargebacks.

Deploy card payments with CentralPay

Our teams analyze your architecture and offer a compliant, ready-to-deploy solution.